Posts

-

Loki Studios, Maker of Location-Aware Mobile Games, Acquired by Yahoo!

Loki Studios, makers of the location-aware mobile game Geomon, has been acquired by Yahoo! according to an announcement on their website.

Loki Studios, makers of the location-aware mobile game Geomon, has been acquired by Yahoo! according to an announcement on their website. The company was cofounded by Ivan Lee, Chris Meill, and Brian Laub and the goodbye note is also signed by Marco, Sam, Gene and Bart. It looks like the 7 person team will join Yahoo’s mobile team. Notably Jessica Lee, the companies UI designer, does not appear to be included in the note so it is unclear whether she will be part of the acquisition.

The Geomon game, their first and only title, was free to download but makes money when users make in-app purchases to improve their characters and purchase other premium experiences. Sources familiar with the company say they had roughly 300,000 users signed up. According to AppData they last shipped an update to the iOS app in July 2012.

Yahoo! has been on a tear with small talent acquisitions this year so far, and PandoDaily’s Erin Griffith wrote a piece titled “Can’t raise a Series A? Just sell yourself to Yahoo” suggesting that many small teams unable to survive the Series A crunch might find safe harbor there. The article goes on to describe common characteristics of companies acquihired by Yahoo!:

Her targets all generally fit the profile of a Series A crunched startup (though obviously I can’t speculate on each of their exact options when they sold). For starters, none has raised a Series A round. Most had accumulated seed funds in the form of a “party round†with long lists of angel investors but no lead investor. All are consumer-facing. None had experienced any truly notable traction before the deal. (Astrid seems to have been the biggest with 4 million users.) Only one or two had a clear path to revenue. All were well-designed by talented teams of fewer than 10 employees. None of their products were particularly revolutionary or even unique in their categories. All of them were shut down and folded into Yahoo’s offerings upon acquisition with hardly a peep of outrage from their users.

Other acquisitions by Yahoo! this year include Stamped, ONtheAir, Snipt.it, Jybe, Summly, Astrid, Milewise, and GoPollGo.

Read the full announcement:

-

Revenue vs. Value

I get a lot of feedback asking why the monthly startup momentum index doesn’t include revenue as a signal. There are two reasons, and the first is that most startups don’t want to provide that data to outsiders. The second is a bit counterintuitive, but stick with me and I’ll explain: revenue doesn’t actually matter for finding hot early stage startups.Startups aren’t supposed to be revenue machines right away; at first they’re designed as business model experiments.

I get a lot of feedback asking why the monthly startup momentum index doesn’t include revenue as a signal. There are two reasons, and the first is that most startups don’t want to provide that data to outsiders. The second is a bit counterintuitive, but stick with me and I’ll explain: revenue doesn’t actually matter for finding hot early stage startups.Startups aren’t supposed to be revenue machines right away; at first they’re designed as business model experiments.While revenue is a useful signal to founders, indicating they are creating something people want, it is also a lagging indicator of success. Startups who are willing to reveal revenue data publicly do so because it reflects well on them. They’re in control of their destiny and decide when and how to raise money. Investors and employees have already missed the window of massive upside that comes with getting in before the company reaches this milestone.

By the time a startup has a predictable and steadily growing revenue stream that means it has built a product and brought it to market successfully, so the risk of investing in it has gone down tremendously and so has the reward. This is why Y Combinator stands to be massively successful – they invest early enough to capture the upside of startups that haven’t figured these things out yet, and then they help them improve and de-risk the company before involving future investors. The YC model tolerates much greater uncertainty than other angel investors and in return they receive outsized gains from big wins, plus minimal losses from companies that fail.

How can we identify these pre-revenue startups with significant upside and get involved in them before this happens? I believe there are many publicly available signals that indicate how a company is doing, and I am building tools to track, measure and organize this information.Revenue First

Early revenue can be dangerously distracting for founders. Once you have some of it you want more, and without strict discipline it’s easy to optimize for immediate gratification rather than the big vision. For founders who have never made $10k a month this feels like a lot of money, especially for the young software engineers straight out of college who never even had salaries that high.

Now in order to make your graph go up and to the right you need to make $12k next month, and $14.5k the next, and $17k the month after that. And that’s just 20% growth month-over-month, which is not actually that sexy of a growth rate – after a year you should have a $87k month in revenue, giving you an annual run rate of just over $1 million. That’s a tiny business, and remember this is revenue not profit. If you run a tight ship this might be break even, but if you’re doing B2B software you probably need to hire support, sales, and lot’s of engineers. You need to raise more money.

What if this same startup, who is seeing steady but not spectacular linear revenue growth, is also fast becoming the most well known new company in its emerging space? They’re discussed on Hacker News all the time, friends have started using them, they’re clever and engaging on Twitter and I see them retweeted all the time, their company blog shows up on Techmeme once in awhile and when their CEO comes to speak at a conference he is the highlight of the event. I’m seeing them everywhere. A couple friends have gone to work there.

These signals, combined with dozens of other more subtle ones reaching me subconsciously, lend the company an air of inevitability.Be everywhere, be awesome.

Capturing Value

How much does this public awareness increase the value of the company? A lot.

As a founder, investor, or employee what matters more? $10,000 in revenue this month or the beginnings of a brand that is known and loved thousands of people and growing every day.When you see unexpected, small, or otherwise questionable companies in my latest top 20 list swallow your cynicism and dig deeper. For investors this is a list of pre-qualified leads worth reaching out to. For knowledge workers these are companies with upside opportunity if you join the team right now. For founders, this is acknowledgement of the hard work you’re putting in pre-revenue to build a massively valuable company.

Don’t let revenue be your vanity metric.

-

Top 20 B2B Startups with the Most Momentum Lead by Disqus, Virool & Bitnami

Last week I published the April index of startups ranked by momentum. But scrolling through hundreds of rows isn’t much fun when all you really want to find the diamonds in the rough, so I thought I’d pull out the top 20 B2B companies with the most momentum right now.The index is built using time series data collected on several signals to create a momentum score combining the footprint of the company and the velocity of changes in the signals. It’s also designed to let consumer and B2B startups to stand on equal footing.

I’ve also included their most recent funding date and round amount. Enjoy and if you have suggestions for startups we should add to the index submit them here.

Full Disclosure: I am an angel investor in Bitnami.

-

Facebook

I told a friend today that I really only use Facebook because I feel obligated for work. It’s true, I don’t read the feed and I don’t spend a ton of time there. I post links to stuff I write and respond to messages and chats, but I am not into the rest of the site at all anymore. I hate the feed, it is overwhelming and takes forever to process. I’ve friended too many people who I barely know and it’s too much work to purge. I just don’t care that much about my Facebook account.

I went to community college briefly and then went straight into the workforce, so when Facebook was sweeping through colleges I wasn’t able to get an account (no college email address). I remember the first time I saw it I was visiting a friend at UC Davis and it had recently come to her campus. I had used Friendster and was really into Livejournal, not that big on Myspace, and Facebook seemed pretty simple. She said everyone was obsessed with it, and I signed up when they made it available to everyone. After I signed up I just kind of ignored my account for 6 months (I would later do this with Twitter too) until one day I got an email saying someone had tagged me in a picture. I came back to see what the picture was, and then I stayed.

Shortly after I got onto Facebook I stopped posting on my Livejournal, eventually deleting it for real (not that I hadn’t deleted it tons of times to “make a statement” as Livejournalers used to do). The Livejournal community had kind of died, it had been bought by some Russian company and lost its soul. I was ready to move on and Facebook was ready to let me in. My Xanga account also lost my interest, and my AngelFire site. I had spent countless hours customizing those websites with my meagre web design skills to be a reflection of my own personality but Facebook offered a simple design centered around what I found most interesting – other people.

Fast forward to today and I use Facebook like everyone else. I share pictures, notes, new stories, participate in groups and try to present myself and express myself in that blue and white world. But I know how much I’ve lost – I have a blog I still update regularly and design myself with open source WordPress.org as the backbone. Everything meaningful goes here, not on Facebook. I know my long term social presence on the web, and in the world, won’t be on Facebook and I house my writing somewhere that I control completely. The server, the code, the design, the word… it’s the real expression of me. And while Facebook has evolved in one way I’ve evolved in another direction, and I don’t want to be inside that box.

I know that the motivation to use Facebook is broken for me because when I put out some new information like a status or a picture and no one comments I’m kind of sad, and then I feel ashamed of the fact I’m even considering filtering what I post based on whether I think it will get a “like”. How shallow!

When I put up a new post on my blog, even if I get no comments, few tweets, few pageviews, I feel good. Writing something and publishing it here feels like making a small creation, revealing a small bit of myself, offering up a tiny sliver of something new that I made today. So I think the next Facebook, at least for me, won’t be Facebook at all. It will be a place where I can control the experience of my visitors and express myself as an individual. It is more like to be Wix, Tumblr, Svtble, Strikingly, Medium, etc than anything dubbed as a “social network”.

Hat tip to Scott Hanselman, who has influenced my thinking on this for awhile and who I can finally relate to first hand. If this post resonates with you please check out his post “Your Words Are Wasted”.

-

HZO Raises $3.6M to Waterproof Pretty Much Anything

It seems the day I take the protective case off my phone is the same day I spill a cup of coffee on it, and adding a case to my beautiful iPhone 5 ruins the beautiful aesthetic.

It seems the day I take the protective case off my phone is the same day I spill a cup of coffee on it, and adding a case to my beautiful iPhone 5 ruins the beautiful aesthetic.While these complaints are definitely first world problem, waterproofing electronics is a big business and according to a regulatory filing HZO has just raised $3.6M more to continue its development of nano-coating technology to waterproof devices.

-

Quincy Jones Raises $682K More For His “Rosetta Stone of Piano” Startup

As someone who loves (and misses) playing the piano, I was excited to see a regulatory filing showing that Playground Sessions has raised $682,275 to continue building the piano lessons software startup.

As someone who loves (and misses) playing the piano, I was excited to see a regulatory filing showing that Playground Sessions has raised $682,275 to continue building the piano lessons software startup.The company is founded by Chris Vance and co-created by Quincy Jones, a living legend in the entertainment industry and recipient of 27 Grammy Awards. The service was launched in February and Jones calls it “the Rosetta Stone of piano”.

After 3 years of hard work, I’m announcing the launch of my new product @playgroundpiano, the Rosetta Stone of Piano. bit.ly/mRPO3R

— Quincy Jones (@QuincyDJones) February 19, 2013

Michale Carney of PandoDaily covered the company in April and I enjoyed his recounting of Jones listening to a David Sides performance intently. As he described it:

“I had the privilege of sitting next to Jones during the performance. For a man who has collaborated with Sinatra, the Beatles, Michael Jackson, and other luminaries, it was inspiring to watch him become engulfed in the music. While he started off quietly, a few turns in Jones was feverishly tapping his foot along with the beat and humming the melody while swaying in his seat. It was the picture of a man squarely in his element.”

Here is a video of that performance:

According to Carney, Sides scored a 99% in the app for the rendition of One Republic’s “Apologize”.

Investors in this round include two agency execs: Andrew Howlett – CDO of Rain and Neil Munn – CEO of Zag at Bartle Bogle Hegarty of London. The company previously raised $160K in October 2012 from these same investors.

Aspiring recording engineers – it’s important to know how to read music – Quincy Jones has a learning tool for that ow.ly/jI9WX

— Womens Audio Mission (@womensaudio) April 3, 2013

Becoming a member of the service costs $9.99/month to access the community and bootcamp materials. From there members received discounts on tutorials and sheet music, which can also be purchased by non-members at a higher price. Members also get access to badging, leaderboards, scoring of their practice and many other social features to encourage them to practice and play.

Not sure who Quincy Jones is? Listen to this barbershop quartet style tribute to The Dude featuring Ludacris, Naturally 7 and Rudy Currency doing “Soul Bossa Nostra”:

-

3D Printing Startup Shapeways Raises Massive $30M Series C

In a regulatory filing Shapeways, the marketplace for 3D printing, revealed the company has raised $30M in a new round of venture funding from Andreessen Horowitz, Union Square Ventures, Index Ventures and Lux Capital. The round was lead by a16z and Chris Dixon has joined the Shapeways board of directors.

In a regulatory filing Shapeways, the marketplace for 3D printing, revealed the company has raised $30M in a new round of venture funding from Andreessen Horowitz, Union Square Ventures, Index Ventures and Lux Capital. The round was lead by a16z and Chris Dixon has joined the Shapeways board of directors.The company enables anyone to design and produce one-of-a-kind bespoke products using 3D printing.

Turns out this was already covered by TechCrunch back in April — oh well! — Shapeways is such a cool company why not write it up again? I personally can’t wait to see what comes next from the New York based company who, according to LinkedIn, now have 70-80 employees. In fact, I’m buying this incredible iPhone 5 “Sweater” case right now.

I still remember the first time I saw one of the products made by them a few years back at SXSW when they were just getting started, and I thought it was a cool thing for hobbyists but didn’t completely understand how it would get big. Turns out things that hobbyists love (ahem Twilio, computers, etc.) can be embraced by a much larger audience, and it looks like Shapeways has figured out how to crack the code and now boasts a marketplace of more than 10,000 stores on their site.

Cool Things Made with Shapeways

Image Credit: Fragatory

Image Credit: Adafruit

Image Credit: http://www.markflorquin.be

Image Credit: retrocactus on Flickr

Image Credit: Shapeways

-

HealthFleet Raising $3M Series B for SaaS Interactive Healthcare Management

According to a regulatory filing HealthFleet, a Boston-based health technology startup, is raising up to $3M in venture capital. The company previously raised a $1.1M Series A in August 2012.

According to a regulatory filing HealthFleet, a Boston-based health technology startup, is raising up to $3M in venture capital. The company previously raised a $1.1M Series A in August 2012.HealthFleet’s platform connects patients with counselors (nurses, nutritionists and other caregivers) and health management content to help manage their health beyond the hospital or doctor’s office.

Founder and CEO Bill Van Wyck has quite a track record for founding companies and taking the public. According to the HealthFleeet about page:

Prior to founding HealthFleet, Mr. Van Wyck founded RedRoller, the ‘Travelocity for shipping packages’ where in 2007 he grew it to a public company (OTCBB:RROL) with over 10,000 users. Prior to RedRoller, Mr. Van Wyck successfully built, operated and sold CSI, a technology integrator, to Elcom International, one of the first ecommerce solution companies. Mr. Van Wyck grew Elcom’s same-region sales from $13MM to $110MM in two years, during which time Elcom completed its IPO (Nasdaq:ELCO). An experienced entrepreneur, Mr. Van Wyck has both public and private company operating experience.

Investors in this and the previous round were not revealed in the funding documents.

-

Tableau Software Ups IPO Amount from $150M to $215M

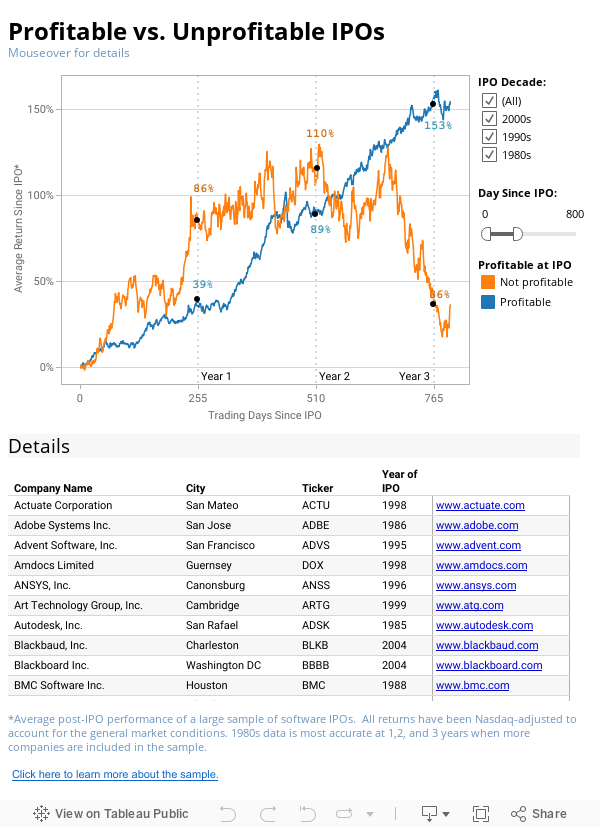

In April we reported that the Tableau Software IPO would be for $150M, but the latest regulatory filings show the company could raise quite a bit more, with the top of the range set at $215M.The Seattle-based company is profitable, earning a net income of $1.4 million in 2012 on revenues of $127.7 million.

In April we reported that the Tableau Software IPO would be for $150M, but the latest regulatory filings show the company could raise quite a bit more, with the top of the range set at $215M.The Seattle-based company is profitable, earning a net income of $1.4 million in 2012 on revenues of $127.7 million.Check out this visualization of post-IPO success (created using Tableau of course) depending on whether or not the company was profitable going into the public market:

-

Clustrix – #5 on YC Startup Index – Raises $16.5M Series C

This morning Clustrix announced they have raised $16.5M in a Series C round from Sequoia Capital, U.S. Venture Partners, ATA Ventures and Don Listwin. They are one of the earliest Y Combinator companies, founded in 2005 with nearly $47 million raised to date. Clustrix was ranked #5 on our Y Combinator Index for April.

This morning Clustrix announced they have raised $16.5M in a Series C round from Sequoia Capital, U.S. Venture Partners, ATA Ventures and Don Listwin. They are one of the earliest Y Combinator companies, founded in 2005 with nearly $47 million raised to date. Clustrix was ranked #5 on our Y Combinator Index for April.The Benefits of MySQL Without the Scaling Limitations

Clustrix scales MySQL databases as engineering operations needs increase, simply by adding more nodes on Amazon Web Services. The company solves parallel processing challenges associated with applications that have a large quantity of data transactions, and is also used by dev ops to get realtime reporting on database performance an automatically scale up our down the number of nodes in use.

Clustrix scales MySQL databases as engineering operations needs increase, simply by adding more nodes on Amazon Web Services. The company solves parallel processing challenges associated with applications that have a large quantity of data transactions, and is also used by dev ops to get realtime reporting on database performance an automatically scale up our down the number of nodes in use.Before Clustrix an entirely different kind of datastore, such as MongoDB, would be used. This requires developers to split up their data across multiple servers and use a map reduce algorithm in order to query across all the data. However, developers using Clustrix save time because they can use their existing application code and MySQL connectors and don’t have to deal with sharding.

Possible IPO In Sight?

A PEHub article covering the announcement says:

CEO Robin Purohit told peHUB that the company will likely raise more funding in the next year to bring it to cash-flow positive. “And then we’ll see where the public markets are,†he said.

We’ll certainly keep an eye out for the next REG D to cross the SEC wire from Clustrix, and keep you posted on their monthly momentum and overall progress in the Startup Index.

Photo Credit: Clustrix Facebook page